Facebook

Facebook

X

X

Pinterest

Pinterest

Copy Link

Copy Link

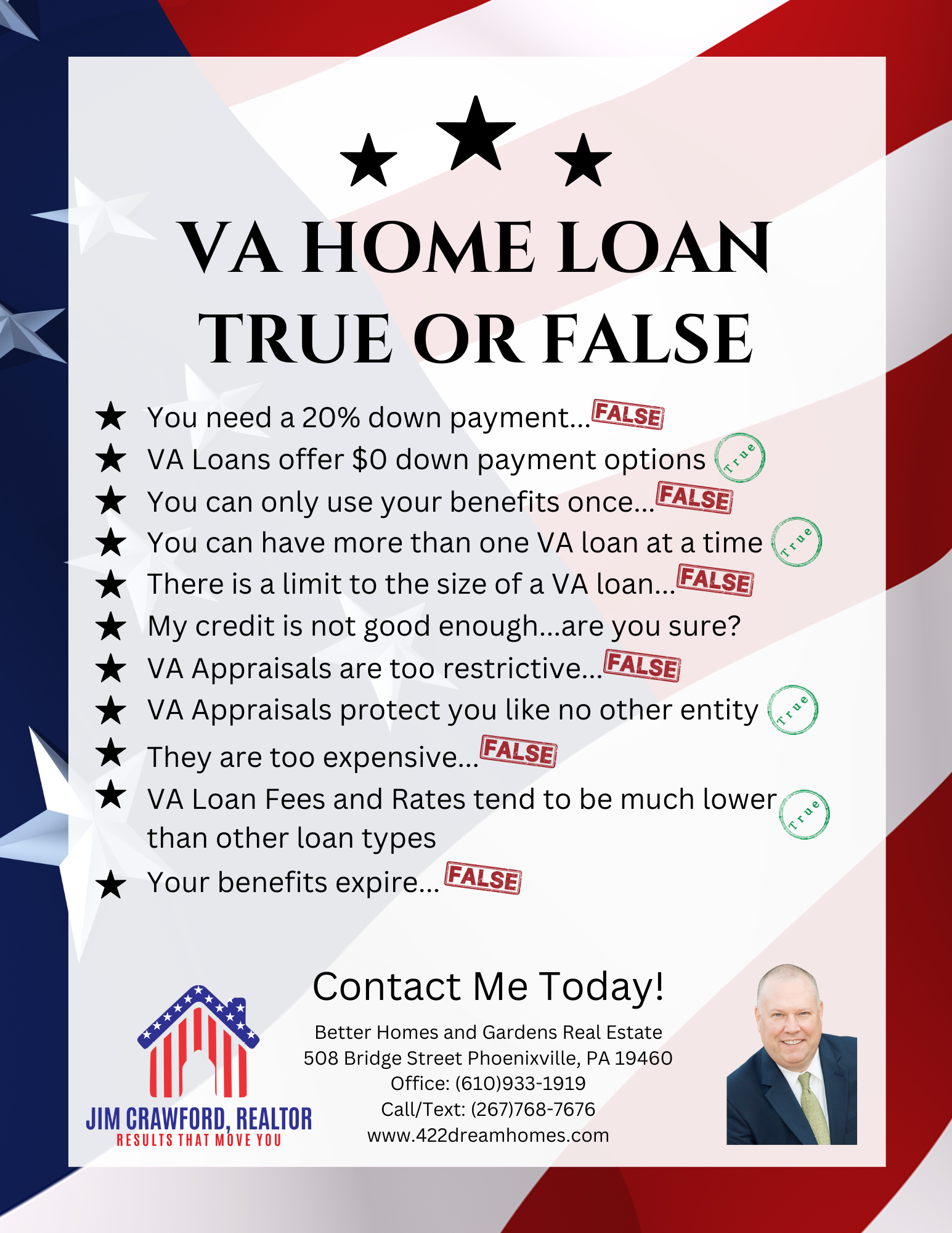

A VA (Veterans Affairs) mortgage loan is a home loan option that is available exclusively to current and former members of the U.S. military. The VA loan program was created in 1944 as part of the GI Bill of Rights to help veterans and their families buy homes without needing a down payment or private mortgage insurance. There are several benefits of VA mortgage loans that make them a great option for eligible borrowers.

- No down payment required One of the biggest advantages of VA loans is that they do not require a down payment. This means that eligible borrowers can purchase a home with no money down, which can be a significant benefit for those who do not have a large amount of savings or cannot afford a down payment.

- No private mortgage insurance (PMI) VA loans do not require private mortgage insurance (PMI), which is typically required for conventional loans when a borrower has a down payment of less than 20%. PMI can add hundreds of dollars to a borrower’s monthly mortgage payment, so not having to pay for it can make a significant difference in the affordability of a VA loan.

- Competitive interest rates VA loans generally offer competitive interest rates, which can help borrowers save money over the life of their loan. In addition, there is no penalty for prepaying a VA loan, which means that borrowers can pay off their loan early without incurring any additional fees or charges.

- Easier qualification requirements VA loans generally have more flexible qualification requirements than conventional loans. For example, borrowers with lower credit scores or a history of bankruptcy or foreclosure may still be able to qualify for a VA loan. In addition, the VA has no minimum credit score requirement, although individual lenders may have their own minimum credit score requirements.

- Closing cost assistance The VA has a program that allows eligible borrowers to receive assistance with closing costs, which can help reduce the amount of money needed to purchase a home. The VA also limits the amount that borrowers can be charged for certain closing costs, which can help make the loan more affordable.

- Assumption option VA loans are assumable, which means that if a borrower sells their home, the new buyer can assume the existing VA loan. This can be a valuable benefit for sellers, as it can make their home more attractive to potential buyers.

In conclusion, VA mortgage loans offer several benefits that can make them an attractive option for eligible borrowers. These benefits include no down payment, no private mortgage insurance, competitive interest rates, easier qualification requirements, closing cost assistance, and an assumption option. If you are a current or former member of the U.S. military, a VA loan may be a great option for you to consider when purchasing a home.